Which states are most at risk for flooding?

The Federal Emergency Management Agency unveiled Risk Rating 2.0 in 2021, and as of April 2023, the new pricing methodology was fully implemented. According to analysis of FEMA data, policies were the most expensive in Connecticut and the least expensive in Alabama.

What states have the highest flash flood losses?

FOX Weather reveals which states have the highest flash flood losses and why.

Flooding can impact nearly the entire country, but some communities are more susceptible than others due to a region’s natural terrain, infrastructure and population.

An analysis of data from the Federal Emergency Management Agency showed that Texas annually sees the most losses due to flooding, with New Jersey and Louisiana ranking second and third, respectively.

FEMA defines the expected annual loss as the average damage in dollars to buildings, population and agriculture.

Flooding is either considered to be riverine or coastal, with each event having unique consequences.

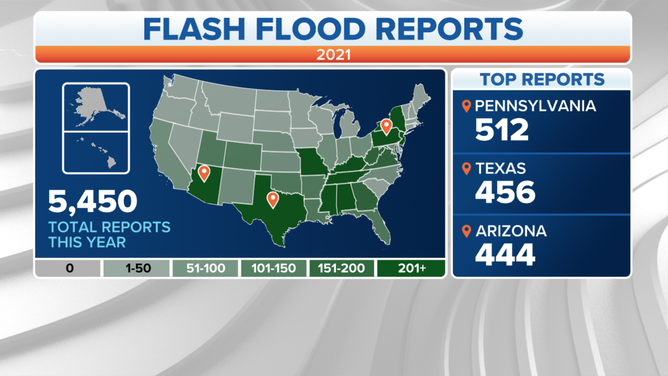

A map showing 2021 flash flood reports in the U.S.

(FOX Weather)

Riverine flooding is caused when waterways exceed their capacity and overflow their banks and is the most common type of flooding.

One of the most devastating floods in modern U.S. history was a riverine flooding event, when the Mississippi River and its tributaries inundated more than 20 million acres across nine states during the summer of 1993.

Coastal flooding events are caused by high tides and surges from storm systems, such as hurricanes.

The frequency and impacts from coastal events are considered to be on the rise due to more Americans moving to seaside communities and climate change.

In 2012, the remnants of Hurricane Sandy impacted the East Coast, with widespread coastal flooding that equated to more than $60 billion in damage.

SOME MAJOR EAST COAST CITIES ARE SINKING AS SEA LEVELS RISE, STUDY FINDS

When coastal flooding and riverine flooding are broken down into two separate entities, New Jersey, New York and Virginia top the list for biggest coastal impacts, while the Lone Star State, Louisiana and California rank highest for the potential of losses during riverine events.

Alaska and several interior states of the Lower 48 rank in the bottom tier of communities that see annual flood events.

When impacts from riverine and coastal flooding are combined, Wyoming typically sees yearly losses of around $7 million, proving that no region is immune from these natural disasters.

Since 1996, FEMA reports it has received flooding claims from 99% of U.S. counties, with more than 40% coming from outside of what are considered high-risk areas.

In high-risk areas, flood insurance is generally required by mortgage lenders, but when outside of the zone, it is usually up to the homeowner whether or not to invest in a policy.

PLAN, PREPARE, PROTECT: HOW TO BEST COVER YOUR PROPERTY AGAINST FLOODS

What is the National Flood Insurance Program?

The NFIP is managed by FEMA and provides renters and homeowners access to insurance to help cover losses incurred due to a rise in tidal waters, runoff, mudslides or erosion.

According to the program, it has roughly 5 million active policies that cover $1.3 trillion in assets.

Two types of coverage are offered for single residences: Building Property (up to $250,000) and Personal Property (up to $100,000.)

The NFIP encourages people to purchase both types, and enrollees may seek additional coverage from private insurers.

There is generally a standard 30-day waiting period after a policy is purchased before the insurance goes into effect.

The average cost of insurance through the NFIP is just over $900 a year, but the amount can vary by state.

According to an analysis of FEMA data, the most expensive state is Connecticut, with an average cost of insurance around $1,590, and the cheapest is Alabama, where the average price is just under $500 per year.